The Bank for International Settlements released its BIS Annual Economic Report 2026 on 28 June, offering a comprehensive assessment of artificial intelligence from both an economic and financial stability perspective. The report identifies AI as a driver of productivity gains while simultaneously highlighting financial vulnerabilities linked to the current investment cycle. Rather than treating these as opposing narratives, the BIS evaluates their interaction and combined implications.

Prepared for central banks, finance ministries and financial regulators, the report outlines four key pressures shaping the global economy in 2026: rapid expansion of AI investment, persistent inflation risks stemming from the Middle East energy crisis, weakening public finances in advanced economies, and rising vulnerabilities in non-bank financial institutions. The BIS emphasises that these developments are interconnected and require coordinated policy responses.

Table of Contents

AI Adoption and Productivity

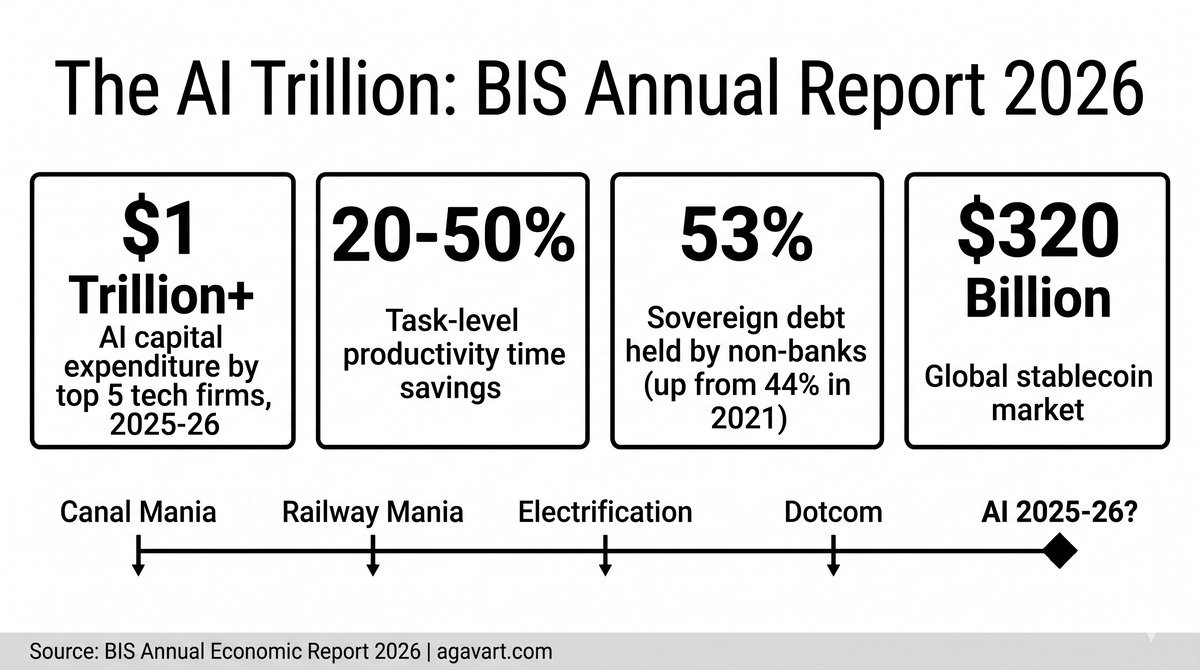

The BIS finds that artificial intelligence is already delivering measurable productivity improvements. Task-level studies cited in the report indicate time savings ranging from 20 per cent to 50 per cent across various professional activities. In the United States, AI-related investment contributed approximately one percentage point to real GDP growth in 2025, marking a significant impact from a single technological domain.

The immediate economic effects have been concentrated in sectors supporting AI infrastructure. Demand for semiconductors has surged, data centre construction has accelerated, and investment in power infrastructure has expanded to meet rising computational needs. Asian manufacturing supply chains, particularly those linked to semiconductor fabrication and electronics assembly, have benefited from increased investment by major technology firms. The BIS also notes that Chinese foreign direct investment into ASEAN economies reached 34 billion dollars in 2024, partly reflecting AI-enabled coordination of regional production networks.

The report further explores a “transformative AI scenario” in which AI systems are capable of self-improvement with minimal human intervention. Under such conditions, innovation would no longer be primarily constrained by human research capacity. While not presented as a forecast, the BIS highlights this as a plausible long-term outcome that current economic and policy frameworks may not be fully equipped to manage.

Financing the AI Investment Cycle

While acknowledging AI’s productivity potential, the BIS Annual Economic Report 2026 draws a clear distinction between the technology itself and the structure of its financing.

The report estimates that the five largest technology firms developing AI infrastructure will invest over one trillion dollars in AI-related capital expenditure during 2025 and 2026. This level of spending exceeds current earnings and free cash flow, leading many firms to rely on increased borrowing. As capital expenditure rises, the BIS estimates that the sector’s net economic surplus, defined as total payoff minus total costs, is declining and could eventually turn negative.

The report also identifies structural risks within the financing model. It highlights “circular financing” arrangements in which chip manufacturers and cloud providers invest in AI laboratories or smaller computing firms that subsequently commit to purchasing hardware or services from the same investors. Such arrangements may create multiple claims on the same underlying assets while offering limited transparency regarding actual risk exposure.

To place current developments in context, the BIS compares the present investment cycle with historical episodes such as Canal Mania, Railway Mania, the electrification boom and the dotcom expansion. In each case, transformative technologies generated long-term economic benefits, but periods of excessive capital investment were followed by financial corrections.

The report also underscores the growing role of non-bank financial institutions in supporting these markets. Hedge funds, private credit funds and similar entities now hold 53 per cent of sovereign debt in advanced economies, up from 44 per cent in 2021. Additionally, 70 per cent of bilateral US dollar repurchase agreements involving hedge funds are conducted with zero haircuts, indicating elevated leverage. The BIS warns that any sharp reassessment of AI-related assets could propagate rapidly through this financial network.

Implications for Emerging Economies

The BIS devotes significant attention to emerging market and developing economies, noting that they face distinct vulnerabilities in the current global environment.

The BIS Annual Economic Report 2026 uses the 2026 Strait of Hormuz disruption as a case study. The temporary closure reduced global crude oil supply by approximately 10 million barrels per day, or about 13 per cent of normal global crude supply by approximately 10 million barrels per day.

The report also raises concerns about monetary sovereignty. Foreign stablecoins now represent a market valued at roughly 320 billion dollars, with 99.4 per cent linked to the US dollar. In economies with weaker confidence in domestic currencies, these instruments may increasingly act as substitutes for local money, reducing the effectiveness of monetary policy and creating additional channels for cross-border capital flows.

A related issue, described as “original sin redux,” concerns sovereign debt markets. Although many emerging economies now issue debt in local currencies, a substantial portion of currency and duration risk is held by foreign investors. During periods of global financial stress and a stronger US dollar, these investors may reduce exposure to local-currency bonds, leading to higher domestic borrowing costs even when shocks originate externally.

Policy Priorities

The BIS groups its policy recommendations into three broad areas.

For central banks, the report emphasises continued vigilance on inflation, particularly second-round effects from higher energy costs. Liquidity support measures should remain temporary, targeted and reversible. The BIS also supports further development of tokenised payment systems that integrate central bank reserves with commercial bank money.

For governments, the report highlights the importance of rebuilding fiscal buffers during periods of stronger growth. It recommends replacing broad-based energy subsidies with targeted household support and promoting investment in workforce skills and competition policies to ensure that AI-driven productivity gains are widely distributed.

For financial regulators, the report advocates “congruent regulation,” whereby institutions performing similar financial functions are subject to comparable regulatory standards regardless of legal structure. It also recommends minimum haircuts for securities financing transactions, expanded use of central clearing in repo markets and stronger prudential standards for stablecoin issuers.

Assessment

The BIS Annual Economic Report 2026 does not present artificial intelligence as a threat to the global economy. Instead, it distinguishes between the long-term economic benefits of AI and the financial risks associated with its current investment structure. The report treats AI’s productivity potential and its financial risks as interconnected, not opposing. Emerging economies are exposed to commodity price shocks and capital flow volatility from this cycle even when they are not primary beneficiaries of AI investment.

For emerging economies, the report carries an additional implication. Many are not primary beneficiaries of current AI investment but remain exposed to commodity price shocks, capital flow volatility and financial spillovers from advanced economies. This underscores the importance of financial resilience and robust policy frameworks during the ongoing phase of AI-led investment.

Frequently Asked Questions: BIS Annual Economic Report 2026

What does the BIS Annual Economic Report 2026 say about AI productivity?

The BIS finds that AI is already delivering measurable gains. Task-level studies indicate time savings of 20 per cent to 50 per cent across professional activities. In the United States, AI investment contributed approximately one percentage point to real GDP growth in 2025, as stated in the report.

What is the $1 trillion AI investment figure about?

The BIS estimates that the five largest technology firms developing AI infrastructure will spend over one trillion dollars on AI-related capital expenditure during 2025 and 2026. This level exceeds current earnings and free cash flow, requiring increased borrowing, according to the report.

What is “circular financing” in AI?

The BIS describes circular financing as arrangements in which chip manufacturers and cloud providers invest in AI laboratories or computing firms that then commit to purchasing hardware or services from the same investors. The report flags this as creating multiple claims on the same assets with limited transparency.

How does the BIS report affect emerging economies like India?

The BIS notes that many emerging economies are not primary beneficiaries of AI investment but remain exposed to commodity price shocks, capital flow volatility and financial spillovers. The report’s case study of the 2026 Hormuz disruption, which pushed fertiliser prices up by 50 per cent and plastic input costs up by 30 per cent, is directly relevant to import-dependent Asian economies.

What does the BIS recommend for financial regulators?

The report recommends “congruent regulation” so that institutions performing similar financial functions face comparable standards regardless of legal structure. It also calls for minimum haircuts on securities financing transactions, expanded central clearing in repo markets, and stronger prudential standards for stablecoin issuers.

Source: Bank for International Settlements, BIS Annual Economic Report 2026, released 28 June 2026. All data and direct quotations are drawn from the primary document. Download Full Report PDF (BIS)

Parallel reading: Stanford University AI Index Report 2026 provides a comprehensive, data-driven overview of AI adoption, investment, research, productivity and global trends. Stanford HAI AI Index 2026

Curated and Reviewed by Deepak Chavan | Founder & Market Expert