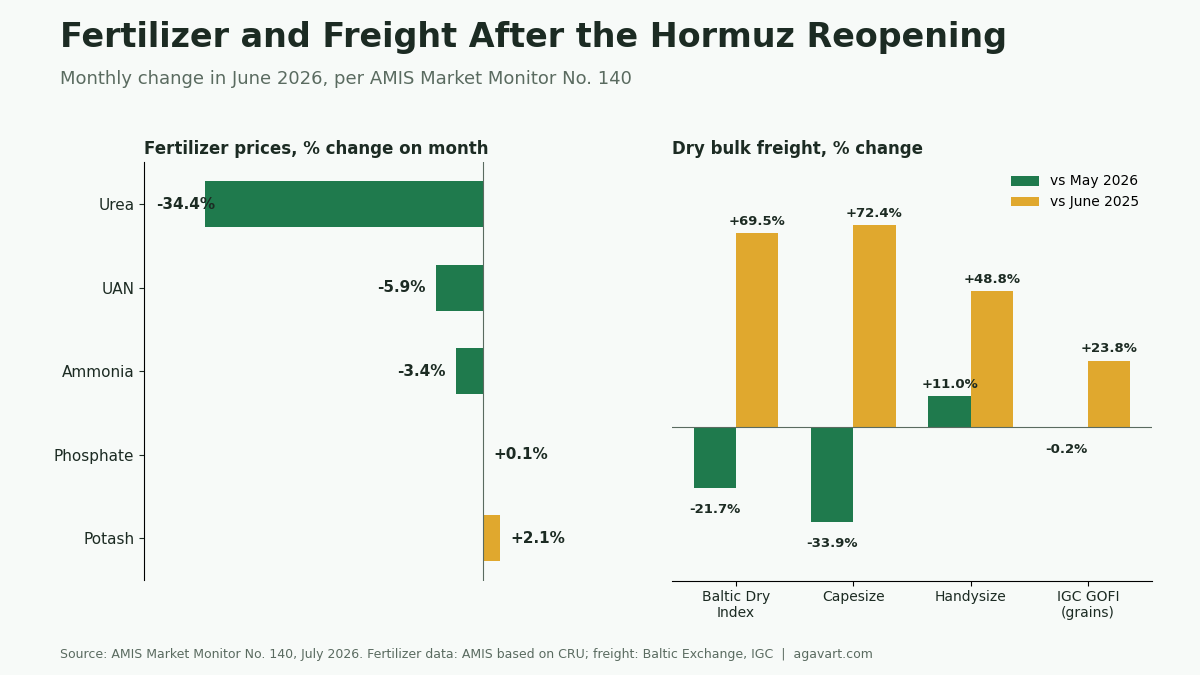

Urea prices fell 34.4 per cent in June as fertilizer flows through the Strait of Hormuz picked up considerably, while phosphate and potash climbed to 12-month highs, according to the AMIS Market Monitor for July 2026. Ocean freight also cooled, with the Baltic Dry Index down 21.7 per cent on the month, though it remains 69.5 per cent higher than a year ago.

The July Monitor, released by the FAO-hosted Agricultural Market Information System, tracks how fertilizer prices and shipping costs are rebalancing after the Iran-United States memorandum of understanding reopened the region’s key shipping chokepoint.

Table of Contents

| Indicator | June 2026 | vs May | vs June 2025 |

|---|---|---|---|

| Urea ($ per tonne nitrogen) | 1,054.9 | -34.4 per cent | +16.5 per cent |

| Ammonia ($ per tonne) | 828.8 | -3.4 per cent | +95.2 per cent |

| UAN ($ per tonne nitrogen) | 1,637.7 | -5.9 per cent | +32.9 per cent |

| Phosphate ($ per tonne P2O5) | 1,878.3 (12-month high) | +0.1 per cent | +17.3 per cent |

| Potash ($ per tonne K2O) | 634.7 (12-month high) | +2.1 per cent | +10.5 per cent |

| Natural gas, US ($ per MMBtu) | 3.2 | +6.9 per cent | -13.1 per cent |

| Baltic Dry Index | 2,524 | -21.7 per cent | +69.5 per cent |

| IGC Grains and Oilseeds Freight Index | 177.5 | -0.2 per cent | +23.8 per cent |

What the AMIS Monitor Says About Fertilizer Prices

June’s fertilizer market was shaped by the Iran-United States memorandum of understanding, which lifted fertilizer flows through the Strait of Hormuz considerably, the report states. Nitrogen led the correction. India’s latest urea tender drew offers exceeding 6 million tonnes against a requested 1.7 million, pushing prices below $450 per tonne CFR and pointing to limited alternative outlets for suppliers. China resumed exports as anticipated, though under quota allocations and shifting price floors. Ammonia weakened as supply constraints in Southeast Asia eased and the United States demand season ended.

Phosphate and potash told the opposite story. Saudi Arabian phosphate exports have yet to normalise, Chinese exports stay constrained, and producers face record-high sulfur costs, keeping fundamentals tight at least into the fourth quarter, as per the report. Potash suppliers reported delivery commitments through August, with China continuing to import significant volumes and modest further gains expected in the coming weeks.

Freight Markets Cool but Stay Elevated

The Baltic Dry Index fell 21.7 per cent in June to 2,524 yet remains nearly 70 per cent above last year. The fall was led by Capesize vessels, whose earnings touched a near two-year peak in early June before rates dropped by around one-third as demand slowed and tonnage availability rose. Panamax rates eased 9.9 per cent, while smaller vessels moved the other way: Supramax rates gained 6.4 per cent and the Handysize index rose 11 per cent on stronger demand at the US Gulf and in the South Atlantic.

Marine fuel prices fell 14 per cent on the month as traffic through the Strait of Hormuz was expected to resume, though the report notes traders suggested trade flows would take time to normalise. The IGC Grains and Oilseeds Freight Index edged down 0.2 per cent, with rates out of Australia dropping 18.8 per cent while Black Sea and European origins firmed.

What Next for Fertilizer Prices and Freight

The report’s outlook hinges on the Strait of Hormuz. Its modelling of the crisis suggests that if the oil price shock proves temporary, fertilizer prices would gradually return towards baseline levels. The pace of recovery in urea flows through the Strait will remain a key driver of near-term prices, while phosphate supply stays tight into the fourth quarter and potash is expected to post modest further gains. For import-dependent buyers, the June numbers mark relief on nitrogen but continued cost pressure on phosphate and potash.

Frequently Asked Questions

Why did urea prices fall in June 2026?

As per AMIS, supply rebounded once fertilizer flows through the Strait of Hormuz picked up, India’s tender drew offers of over 6 million tonnes against 1.7 million sought, and China resumed exports under quotas. Urea fell 34.4 per cent on the month.

Why are phosphate and potash prices at 12-month highs?

Saudi Arabian phosphate exports have not normalised, Chinese exports remain constrained and sulfur costs are at record highs, the report states. Potash suppliers hold delivery commitments through August while China keeps importing.

What is the Baltic Dry Index and why did it fall?

The Baltic Dry Index tracks the cost of moving raw materials by sea. It fell 21.7 per cent in June mainly because Capesize vessel rates dropped by about one-third from a near two-year peak, per Baltic Exchange data in the report.

Will fertilizer prices keep falling?

The report says the outlook hinges on the Strait of Hormuz. Nitrogen could ease further if flows normalise, but phosphate supply stays tight at least into the fourth quarter and potash is expected to edge higher in the coming weeks.

Parallel Reading

Agavart has also covered the SBI Research report on India’s declining oil intensity after the West Asia crisis and the geopolitics of grain in the US-Iran asset dispute, both of which map the same shock from different angles.

Primary Reports and Sources

- AMIS Market Monitor No. 140, July 2026, Agricultural Market Information System (fertilizer indicators AMIS based on CRU; freight data Baltic Exchange and IGC): 📥 Download Full Report PDF

Curated and Reviewed by Deepak Chavan | Founder & Market Expert