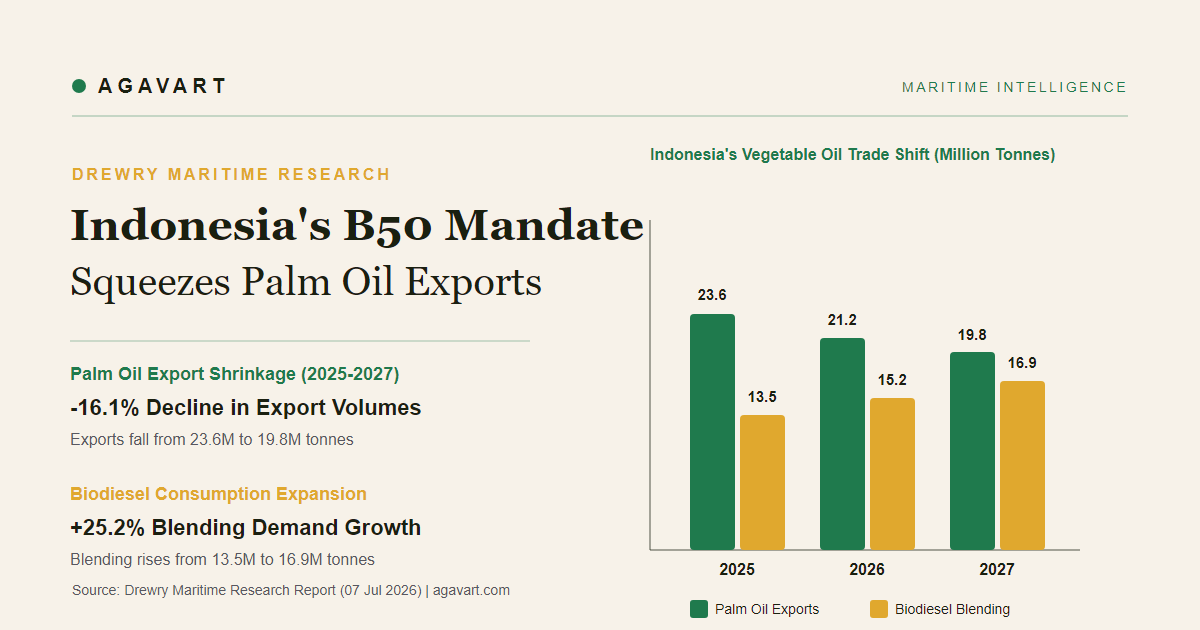

LONDON: The implementation of Indonesia B50 biodiesel mandate from 1 July 2026 is projected to significantly reduce the country’s palm oil exports, creating a major headwind for intra-Asian vegoil shipping freight rates. According to a report by London-based Drewry Maritime Research, Indonesia’s crude and refined palm oil exports are expected to drop from 23.6 million tonnes in 2025 to 21.2 million tonnes in 2026, and decline further to 19.8 million tonnes in 2027. This export squeeze, combined with a rapidly expanding fleet of IMO-class coated tankers, will keep vegoil freight rates on regional Asian routes under downward pressure through 2027.

Report Snapshot

- • The finding: As stated in the report, Indonesia’s B50 biodiesel mandate is projected to squeeze palm oil exportable surplus, depressing regional vegoil freight rates through 2027.

- • By the numbers: Crude and refined palm oil exports are estimated to drop from 23.6 million tonnes in 2025 to 21.2 million tonnes in 2026, and decline further to 19.8 million tonnes in 2027; biodiesel blending demand rises to 16.9 million tonnes by 2027.

- • Why it matters: The policy drives a structural shift in global vegoil flows, reducing shipping demand on regional Asian routes while increasing long-haul soybean oil shipments from Latin America.

- • Source: Drewry, Indonesia’s B50 biodiesel mandate to put pressure on vegoil freight rates through 2027, 7 July 2026, Drewry Maritime Research.

Rising domestic consumption drives export squeeze

The core driver behind the decline in Indonesia’s palm oil exports is the government’s aggressive biodiesel blending program. Indonesia introduced palm oil-based biodiesel blending in 2008 with a modest B2.5 mandate to limit its reliance on imported fossil diesel. Since then, the country has systematically raised the threshold. Following the successful implementation of the B40 mandate in January 2025, the B50 mandate was launched on 1 July 2026. This transition is expected to increase domestic palm oil consumption for biodiesel production by 3.0 to 3.5 million tonnes annually.

According to official data, Indonesia will require 19.7 million kilolitres of palm oil-based biodiesel annually under the B50 mandate, compared with 15.6 million kilolitres under B40. Drewry’s estimates suggest that actual biodiesel blending demand will expand from 13.5 million tonnes in 2025 to 15.2 million tonnes in 2026, and reach 16.9 million tonnes in 2027. Biodiesel consumption accounted for only 13 per cent of total Indonesian palm oil output in 2019, rising to 27 per cent in 2025. Under the B50 regime, this share is projected to jump to 31 per cent in 2026 and hit 34 per cent in 2027.

At the same time, Indonesia’s palm oil production is projected to remain stagnant over the next two years. Yield improvements from newer plantations are expected to be offset by declining output from older, ageing estates. This combination of rising domestic biodiesel mandates and stagnant production limits the country’s exportable surplus, causing exports of crude and refined palm oil to fall from 23.6 million tonnes in 2025 to 19.8 million tonnes in 2027.

Widening tanker fleet capacity vs. regional demand

This export squeeze is set to collide with a rapid expansion in tanker fleet capacity. The supply of IMO-class coated tankers is growing rapidly, with a substantial volume of newbuild deliveries scheduled through 2027. As export volumes of palm oil from Indonesia to major Asian destinations like India and China contract, regional shipping demand for vegoil carriers will fall. With vessel supply rising and demand on intra-Asian shipping lanes weakening, freight rates for regional carriers are expected to face persistent downward pressure.

Long-haul soybean oil flows as a partial offset

However, the global vegetable oil market is highly interconnected. The reduction in Indonesian palm oil exports is expected to tighten global supply and support palm oil prices, narrowing the traditional price discount of palm oil relative to alternative vegetable oils. A narrow price spread between palm oil and soybean oil will likely encourage major buyers like India to increase long-haul soybean oil imports from Latin America (South America) to Asia in the second half of 2026. This shift toward longer-distance trade routes will provide some support to global shipping by increasing tonne-mile demand, helping to cushion the broader decline in vegoil freight rates.

Frequently Asked Questions

1. How much palm oil will Indonesia consume for biodiesel under B50?

The B50 mandate requires 19.7 million kilolitres (approximately 16.9 million tonnes) of palm oil-based biodiesel annually, representing an increase of 3.0 to 3.5 million tonnes in domestic consumption over B40.

2. By how much will Indonesia’s palm oil exports decline?

Drewry estimates that Indonesia’s palm oil exports will decline from 23.6 million tonnes in 2025 to 21.2 million tonnes in 2026, before falling further to 19.8 million tonnes in 2027.

3. Why are vegoil freight rates on regional routes expected to fall?

The combination of declining regional export shipments from Indonesia and the rapid expansion of the IMO-class coated tanker fleet will create an oversupply of vessels on intra-Asian routes, leading to bearish freight rates through 2027.

Source: Drewry Shipping Consultants Limited, London. Original Opinion Article: Indonesia’s B50 biodiesel mandate to put pressure on vegoil freight rates through 2027.

Curated and Reviewed by Deepak Chavan | Founder & Market Expert