The 140 Bcm Ghost Supply is the defining energy shock of 2026. Europe’s latest energy security audits and international gas forecasts carry one blunt warning: the global gas supply chain is undergoing a permanent structural division. The IEA Gas Market Report Q3-2026 warns that the de facto closure of the Strait of Hormuz has triggered a decade-long reorganisation of Western industrial policy. The era of cheap, transition-bridge LNG is effectively dead, replaced by a permanent geopolitical discount on Middle Eastern energy.

Report Snapshot

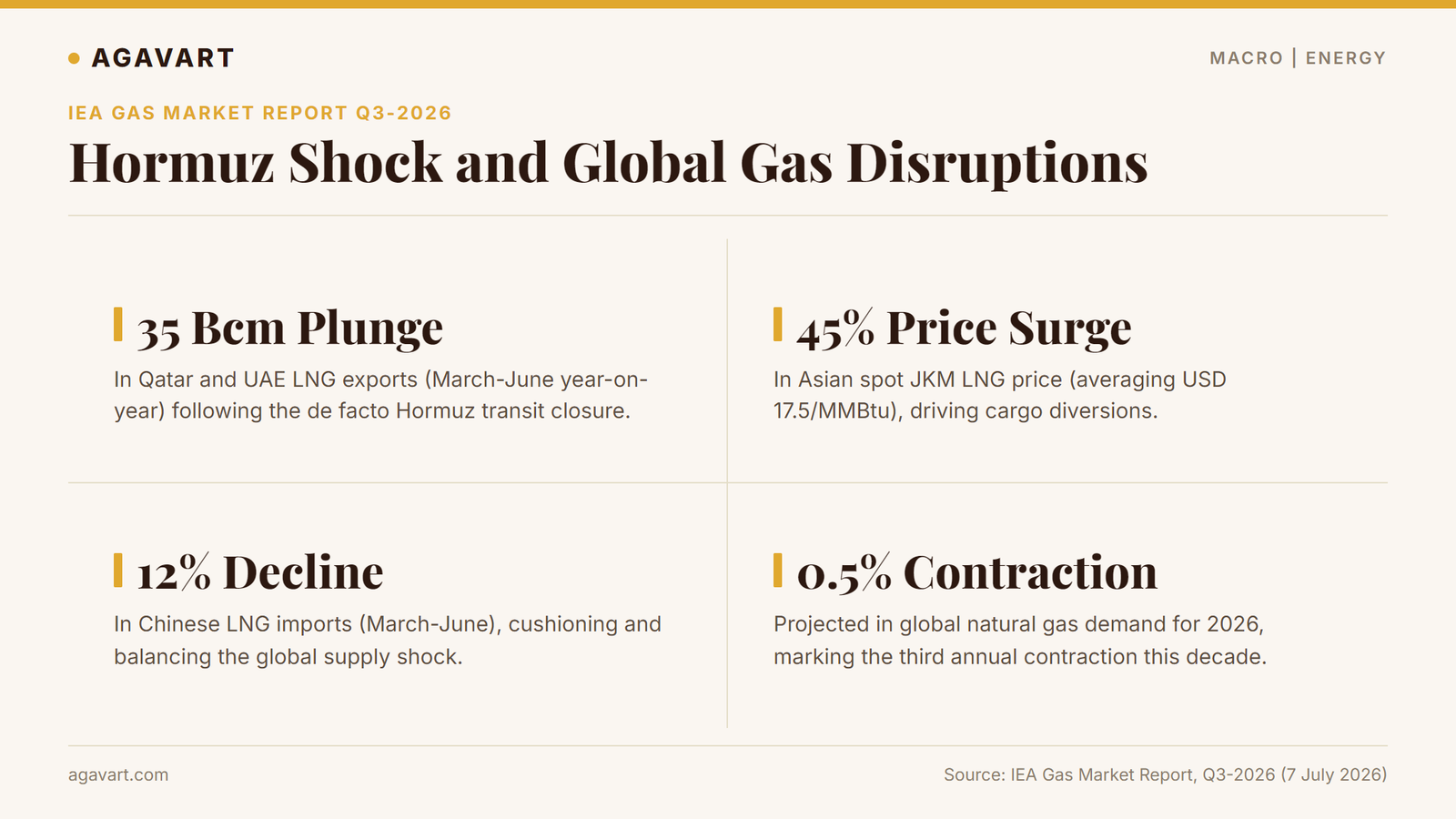

- The finding: As stated in the report, the Middle East conflict and the closure of the Strait of Hormuz have dealt a major supply shock to global natural gas markets, causing high price volatility and a projected 0.5 percent contraction in global gas demand for 2026.

- By the numbers: Qatar and UAE LNG loadings fell by 35 Bcm; Non-Gulf LNG production grew by 18 percent (27 Bcm); Asian spot JKM surged 45 percent (to USD 17.5/MMBtu); Chinese LNG imports fell 12 percent.

- Why it matters: As stated in the report, these supply disruptions have distorted global energy and fertiliser markets, forcing Asian power sectors back to coal and halting nitrogen-based fertiliser exports.

- Source: International Energy Agency (IEA), Gas Market Report, Q3-2026, 7 July 2026. View the official PDF

Table of Contents

If you have a moment, read on for the full breakdown and sources

Table of Contents

- The 140 Bcm Supply Hole: Why Energy Bills Won’t Fall Until 2030

- The Death of the Middle East Reliability Premium

- The New Security Architecture: The Oil-ification of Gas

- Frequently Asked Questions

- Sources and Citations

1. The 140 Bcm Ghost Supply Void: Why Energy Bills Won’t Fall Until 2030

The most startling figure in the Q3-2026 report is the cumulative loss of 140 billion cubic metres (Bcm) of LNG supply projected between 2026 and 2030. To put that in perspective, 140 Bcm is roughly equivalent to the total annual gas consumption of Germany and Italy combined.

The expected supply wave has become a 140 Bcm Ghost Supply void. The report reveals that damage to Qatar’s Ras Laffan liquefaction trains is so severe that repairs will take three to five years, erasing 15 percent of all new global LNG capacity expected this decade.

For Europe, this means a future of high-for-longer prices. The Dutch TTF (European gas benchmark) has seen volatility surges of up to 170 percent. The promised price relief for 2027 is now mathematically impossible. Eurozone industrial giants must accept that feedstock costs will remain 3x to 4x higher than their American counterparts.

For North America, the 140 Bcm Ghost Supply void creates an export tug-of-war. With the world desperate for non-Middle Eastern gas, US LNG projects like Plaquemines are being pushed to 104 percent utilisation, testing the ceiling of domestic Henry Hub prices.

2. The Death of the Middle East Reliability Premium

For thirty years, global energy security rested on a simple assumption: the Persian Gulf is a stable, permanent tap. Even during the 2022 Ukraine crisis, Qatar was seen as the risk-free bank of gas. The Q3-2026 report shatters this mirage, showing a 40 percent drop in Qatari production and a 75 percent drop in regional exports during the peak crisis.

We are now entering the era of the Great Atlantic Pivot, driven directly by the 140 Bcm Ghost Supply shock. Long-term buyers in Berlin, Tokyo, and London are no longer prioritising price. They are prioritising transit risk. Since March 2026, every major Final Investment Decision (FID) has shifted to the Atlantic Basin. The US authorizations for Elba Island and Plaquemines to increase exports indicate that the West is building a Fortress Atlantic energy loop.

This shift is permanent. Even when the Strait of Hormuz fully reopens, the 140 Bcm Ghost Supply deficit will continue to shape investor decisions for years. The reliability premium of the Middle East has evaporated. Investors are pricing in a permanent geopolitical discount on Gulf-based energy, to the benefit of the North American shale patch and the emerging LNG hubs of West Africa (Senegal, Mauritania, and Congo).

3. The New Security Architecture: The Oil-ification of Gas

Perhaps the most significant long-term shift in the report is the institutionalisation of gas security. The IEA Working Party on Natural Gas and Sustainable Gases Security (GWP) is effectively becoming the central bank of gas.

We are moving toward mandatory strategic gas reserves. Europe’s struggle to fill storage (noted as being 23 percent below the five-year average in mid-2026) has proven that market forces alone cannot guarantee winter survival.

This means state-led storage funding to decouple national survival from daily spot price volatility. It also means a return of coal and nuclear power. The report’s spotlight on gas-to-coal switching shows that even green nations like the Netherlands and France have been forced to relax coal-fired restrictions. In the energy trilemma (Security, Equity, Sustainability), security is now the absolute priority.

Frequently Asked Questions

What is the significance of the 140 Bcm supply hole?

The 140 Bcm Ghost Supply represents the cumulative volume of LNG supply erased from global projections between 2026 and 2030 due to Qatari liquefaction train damage and Hormuz disruptions.

Why did natural gas prices rise in Asia and Europe?

The de facto closure of the Strait of Hormuz blocked Qatari and UAE shipments, removing nearly 20 percent of global LNG supply from active trade and causing Asian JKM spot prices to surge by 45 percent.

What is the Great Atlantic Pivot?

It is the structural shift of global LNG investment and trade flows away from the Persian Gulf and toward the Atlantic Basin (specifically the US and West Africa) to avoid geopolitical transit risks.

Sources and Citations

- International Energy Agency (IEA), Gas Market Report, Q3-2026, published 7 July 2026. View the official PDF

- S&P Global Platts Connect, Platts JKM Pricing Data, March to June 2026.

- CME Group, Dutch TTF Natural Gas Settlements, June 2026.

Curated and Reviewed by Deepak Chavan | Founder & Market Expert