The Federal Reserve July 2026 Monetary Policy Report describes a business credit market moving at two speeds. Large companies, led by publicly traded technology firms funding artificial intelligence, are raising money cheaply in robust bond markets. Small businesses, by contrast, face restrictive bank lending and are leaning more on high-cost credit cards. The report frames this as a widening divide in who can borrow, and on what terms.

Table of contents

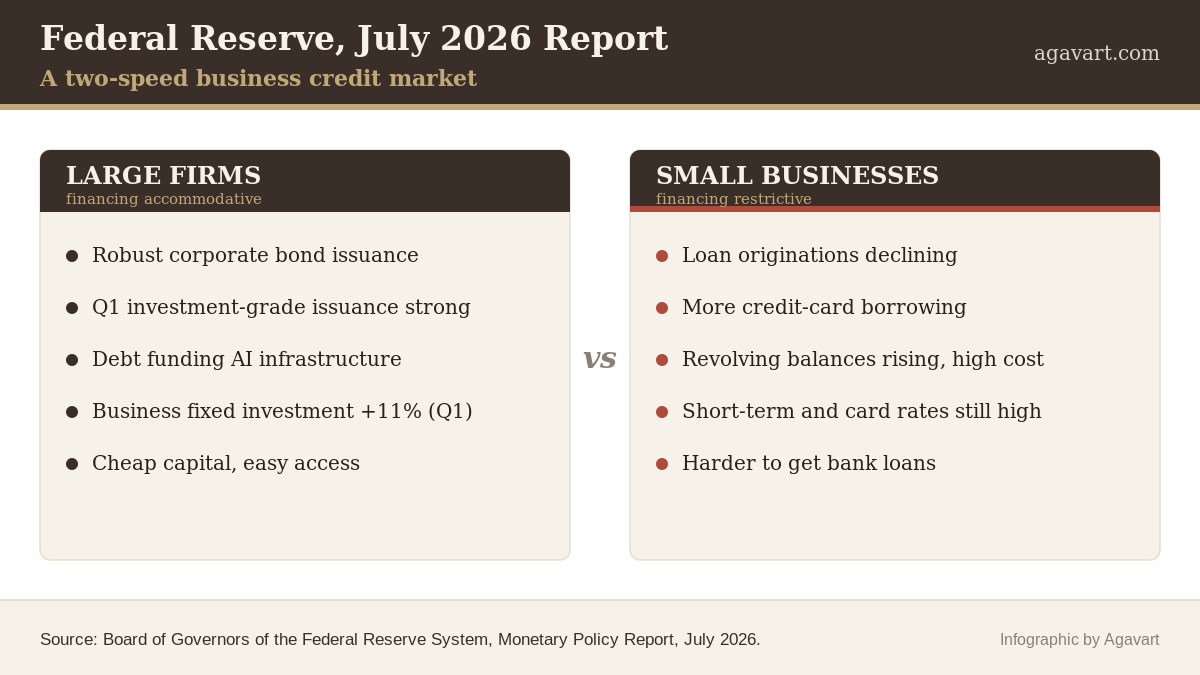

What the report shows

The Federal Reserve’s July 2026 Monetary Policy Report sets out a business credit market split in two. For large companies, financing conditions remained generally accommodative, including in capital markets. Gross issuance of nonfinancial corporate bonds continued at a robust pace through the first half of the year, and net issuance of investment-grade bonds was particularly strong in the first quarter. The report attributes much of that strength to large, publicly traded technology firms, which increased their debt financing of artificial intelligence infrastructure. That borrowing has fed a wider investment boom: business fixed investment rose at an annual rate of 11 per cent in the first quarter, after 5.5 per cent in 2025, with most of the strength connected to building the data centres that support AI services.

Why small firms are on the other side

For small businesses, the picture is close to the opposite. The report describes their financing conditions as somewhat restrictive. Loan originations declined on net, while credit card borrowing by businesses rose steadily through the first half of the year. The report reads the increase in revolving balances on small business credit card debt, a high-cost form of credit, as a sign that these firms have been finding it difficult to obtain loans or credit lines from banks. Interest rates on short-term loans and credit cards fell somewhat in 2026 but, as the report notes, remain high by the standards of recent years. Short-term delinquency rates, having eased earlier in the year, have begun to tick up again.

What it means next

The report does not present this as a crisis, and it notes that a weakening in investor sentiment in private credit markets spilled over into broader credit only to a limited extent. But the divide it describes matters for the shape of the recovery. When the cheapest capital flows to the largest firms building AI, and the smallest firms lean on credit cards to bridge the gap, the benefits of accommodative markets are unevenly shared. Small businesses account for a large share of employment, so their access to affordable credit shapes hiring and investment well beyond the firms themselves. The report’s own signal to watch is the level of small business revolving balances and short-term delinquencies: if they keep rising, it would point to a deepening squeeze on smaller borrowers rather than an easing one.

Frequently asked questions

What did the Federal Reserve July 2026 report say about business credit?

It said business financing conditions have been uneven. Large firms, especially technology companies funding artificial intelligence, enjoyed accommodative conditions and robust bond issuance, while small businesses faced restrictive lending, declining loan originations and rising credit card use.

Why are small businesses using more credit cards?

The report reads the rising revolving balances on small business credit cards, a high-cost form of borrowing, as a sign that small firms have found it difficult to obtain ordinary loans or credit lines from banks.

Where can I read the Federal Reserve July 2026 Monetary Policy Report?

The full report is available free from the Board of Governors of the Federal Reserve System at the link in the source line below.

Parallel reading

- World Bank China Economic Update July 2026: Growth Slows to 4.4 per cent

- IMF World Economic Outlook Update July 2026

Source: Board of Governors of the Federal Reserve System, Monetary Policy Report, July 2026. Download the full report.

Curated and Reviewed by Deepak Chavan | Founder & Market Expert