Europe’s latest research digest and international market forecasts carry one blunt message: spatial inequality and labour restrictions are reshaping productivity. The OECD Employment Outlook 2026 warns that persistent geographic divides, post-employment non-compete clauses, and structural skill mismatches represent hidden structural frictions. These local bottlenecks are actively suppressing aggregate productivity and distorting consumer purchasing power across developed economies.

OECD Employment Outlook 2026 policy calendar: the 2026 to 2030 regional disparities and post-employment restraints review briefings

Report Snapshot

• The finding: As stated in the report, persistent regional gaps in employment rates and disposable incomes continue to divide OECD economies, with technological and trade shocks causing long-term structural joblessness rather than smooth sector transitions.

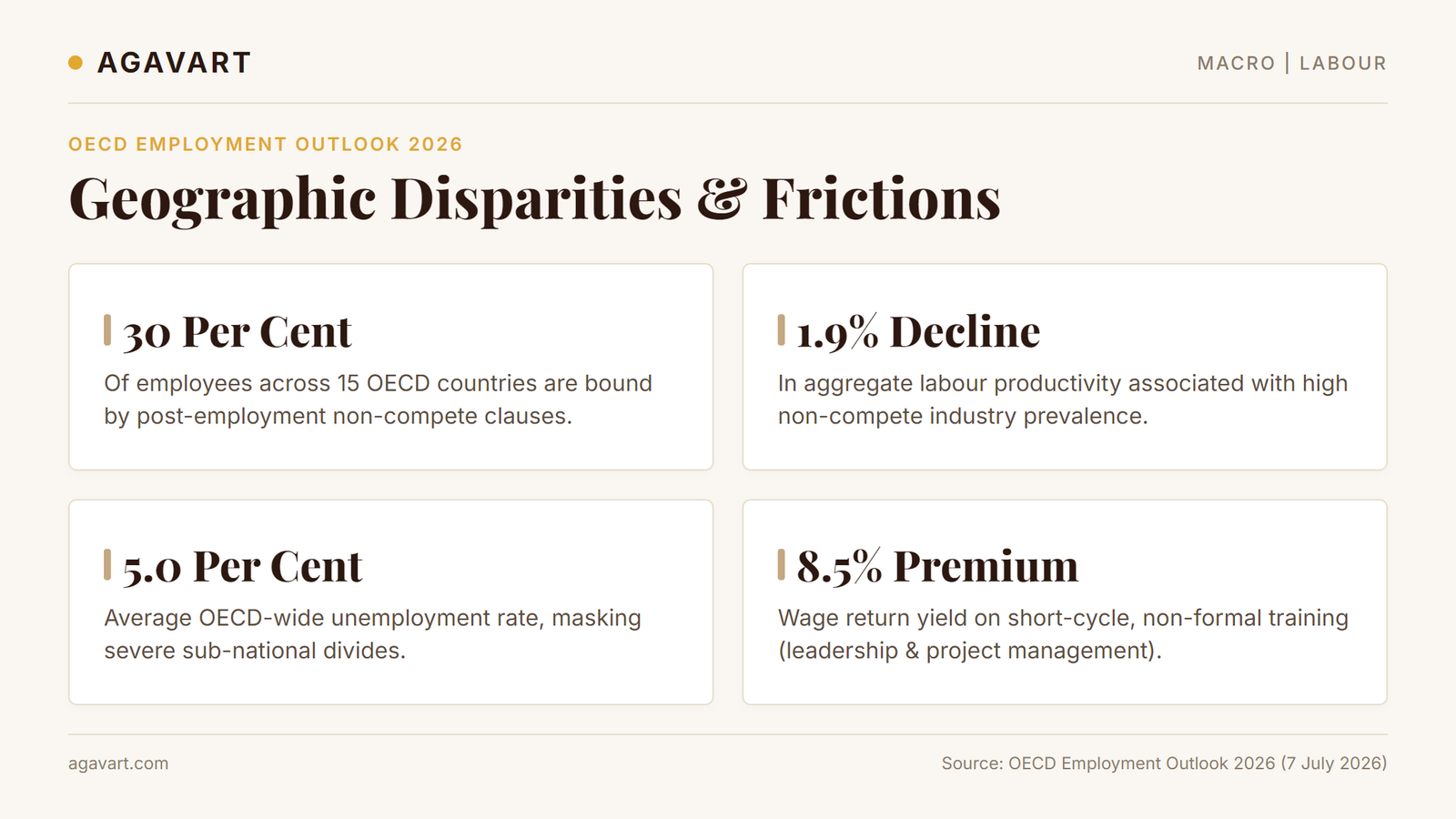

• By the numbers: OECD average unemployment rate held steady at 5.0 per cent; low-unemployment economies recorded rates under 3.0 per cent; high-unemployment economies persisted in double digits; 30 per cent of employees bound by non-competes; 1.9 per cent drop in productivity linked to non-compete prevalence; upskilling courses yield an 8.5 per cent wage premium.

• Why it matters: As stated in the report, spatial divides and post-employment restrictions are eroding aggregate labour productivity and distorting consumer purchasing power, requiring a pivot to place-based policies.

• Source: OECD, OECD Employment Outlook 2026: Geographic Disparities in Jobs and Incomes, 7 July 2026

If you have a moment, read on for the full breakdown and sources

Table of Contents

1. What has changed and the spatial mobility paradox

2. Why regional divides and non-competes are widening the friction

3. What this means, and what to watch

4. Frequently asked questions

Key dates from the outlook

7 July 2026: OECD Employment Outlook 2026 officially launched in Paris.

2016: Graduate youth unemployment rates began rising relative to general working-age cohorts (pre-dating the LLM revolution).

February 2022: The OECD average unemployment rate settled at the historic low of 5.0 per cent.

What has changed and the spatial mobility paradox

The July 2026 survey opens with a warning regarding sub-national divergence. The composite OECD unemployment rate remains anchored at 5.0 per cent, a historic low maintained since early 2022. However, this average masks extreme divergence between member states and their internal regions. Low-unemployment nations like Japan, South Korea, Poland, Mexico, and Israel are operating with jobless rates below 3.0 per cent, bordering on labour shortages. In contrast, countries like Spain and Finland continue to struggle with double-digit unemployment. Crucially, the Outlook notes that these divides are local. Within individual countries, employment rates and average disposable incomes in lagging regions are failing to catch up with metropolitan hubs, trapping workers in low-mobility cycles.

Traditional economic theory suggests that labour mobility acts as a natural stabilizer: workers leave low-opportunity areas for high-growth hubs, eventually equalizing wages. The OECD 2026 data presents a much darker reality. The report finds that those who move are overwhelmingly the best candidates: younger, more educated, and highly adaptable. When these individuals leave a lagging region, the local human capital base erodes so significantly that the region becomes structurally toxic to new investment. This creates a brain drain trap where the probability of an educated individual leaving a low-employment region is 5 percentage points higher than those with lower schooling.

Why regional divides and non-competes are widening the friction

The OECD points to structural economic shifts, including trade adjustments and the rapid deployment of artificial intelligence, as primary drivers of these disparities. While these forces create high-skill service roles in metropolitan centres, they frequently displace manufacturing and routine administrative jobs in industrial and rural regions. Importantly, the adjustment process is not functioning smoothly. Rather than displaced workers successfully retraining and transitioning to growing sectors, they are disproportionately falling into long-term joblessness or dropping out of the active workforce entirely. The report emphasizes that regional mobility is not a cure-all; expecting workers to relocate from depressed areas to high-cost hubs often drains talent from lagging regions while worsening housing pressures in productive cities.

Perhaps the most startling section of the report concerns post-employment restraint clauses. For decades, investors viewed non-compete agreements as a way for firms to protect intellectual property. The 2026 Outlook suggests they have become a major impediment to aggregate productivity. The report reveals that 30 per cent of employees across 15 OECD countries are bound by non-compete clauses. More shockingly, these clauses have moved far beyond the executive suites and research laboratories. They are now pervasive in low-wage, low-skill sectors where no trade secrets exist. The report identifies a chilling effect: even when these clauses are legally unenforceable, workers still refuse to switch jobs out of fear of legal litigation.

Finally, the report warns of a growing regulatory dualism. As countries tighten employment protection legislation for permanent workers, firms are pivoting to on-call or zero-hour contracts. Recent reforms in Spain and Portugal aimed at reducing temporary work have actually led to the rise of open-ended intermittent contracts. These provide the illusion of job security but offer zero guarantee of hours or income. For the investor, this creates a volatile labour supply. Firms relying on these contracts may look stable on paper, but they are exposed to high social and political risks as governments increasingly target false self-employment on digital platforms.

What this means, and what to watch

Everything above is drawn from the OECD Employment Outlook 2026. What follows is Agavart’s analysis, drawing on official sources published since the outlook. Facts and interpretation are kept separate on purpose.

The GDP divergence is a retail trap. The report shows that regional disparities in disposable household income are 3.5 times narrower than disparities in GDP per capita. High regional GDP often reflects where corporate profits are recorded or where commuters create value, not where wealth is actually retained and spent by residents. In developed markets like Austria, Belgium, and the Netherlands, high-GDP regions often house the lowest-income residents due to high housing costs and urban-rural wealth transfers. Investors must pivot their retail and consumer models from regional GDP to equivalised disposable household income to identify true purchasing power.

The productivity impact of non-competes. The data suggests that post-employment non-compete clauses act as a hidden tax on economic dynamism. A 10-percentage-point increase in the prevalence of non-competes within an industry is associated with a 1.9 per cent decline in aggregate labour productivity. As the United States Federal Trade Commission and European regulators move toward banning these restrictive covenants, investors should prepare for a mobility rebound. Industries previously locked down by non-competes will experience a temporary surge in staff turnover, followed by a substantial acceleration in innovation, knowledge sharing, and startup formation.

The human capital return shift. The report indicates a significant shift in the return on investment of human capital. While formal degrees remain essential for entering the labour market, their influence on long-term wage growth is weakening. Short-cycle, non-formal, job-related training is now yielding higher wage premiums in certain sectors than additional years of formal schooling. Specifically, training focused on leadership, teamwork, and project management shows a wage premium exceeding 8.5 per cent. In an era of shrinking workforces due to demographic ageing, the ability of a firm to manufacture its own skills through internal, short-cycle training is a critical competitive advantage that investors must prioritize when evaluating management quality.

Why the reader should care: The OECD Employment Outlook 2026 signals the end of the place-blind investment era. National growth no longer lifts all boats; it elevates a few superstar cities while leaving peripheral regions in structural decline. The labour market is no longer a single liquid pool, but a collection of hyper-local, highly friction-filled ecosystems. Institutional investors who discount national aggregates, bet on firms that reject non-competes, and prioritize internal corporate upskilling will capture the highest returns in an otherwise low-growth global economy.

Frequently Asked Questions

What is the current OECD average unemployment rate?

As of the release of the 2026 Outlook, the average OECD unemployment rate stands at 5.0 per cent. It has remained at this historic low since February 2022, though country-level rates vary from under 3.0 per cent to double digits.

What is the main theme of the OECD Employment Outlook 2026?

The 2026 report is subtitled “Geographic Disparities in Jobs and Incomes” and focuses on how spatial divides and regional inequality shape employment opportunities and income mobility across member states.

Why is worker mobility insufficient to solve regional job gaps?

The OECD warns that relying on workers relocating to high-employment regions can drain skills and young talent from lagging communities, while increasing cost-of-living and housing pressures in major metropolitan areas.

Sources and further reading

Primary source: OECD, OECD Employment Outlook 2026 (7 July 2026): OECD iLibrary Portal

Supporting context (Agavart analysis):

OECD Data Explorer, Labour Market Statistics: data.oecd.org

United States Federal Trade Commission, Non-Compete Clause Rule: ftc.gov

Curated and Reviewed by Deepak Chavan | Founder & Market Expert